As we step into 2025, the Santa Clara County real estate market continues to evolve, presenting new opportunities and challenges for buyers, sellers, and investors alike. Known for its dynamic housing landscape, this region remains a key focal point in California’s real estate scene. In this blog, we’ll explore the latest market trends, key metrics, and insights shaping the year ahead. Whether you’re looking to buy your dream home, sell your property, or simply stay informed about the local market, this guide provides valuable data and analysis to help you navigate 2025 with confidence. Let’s dive into the numbers and trends that matter most!

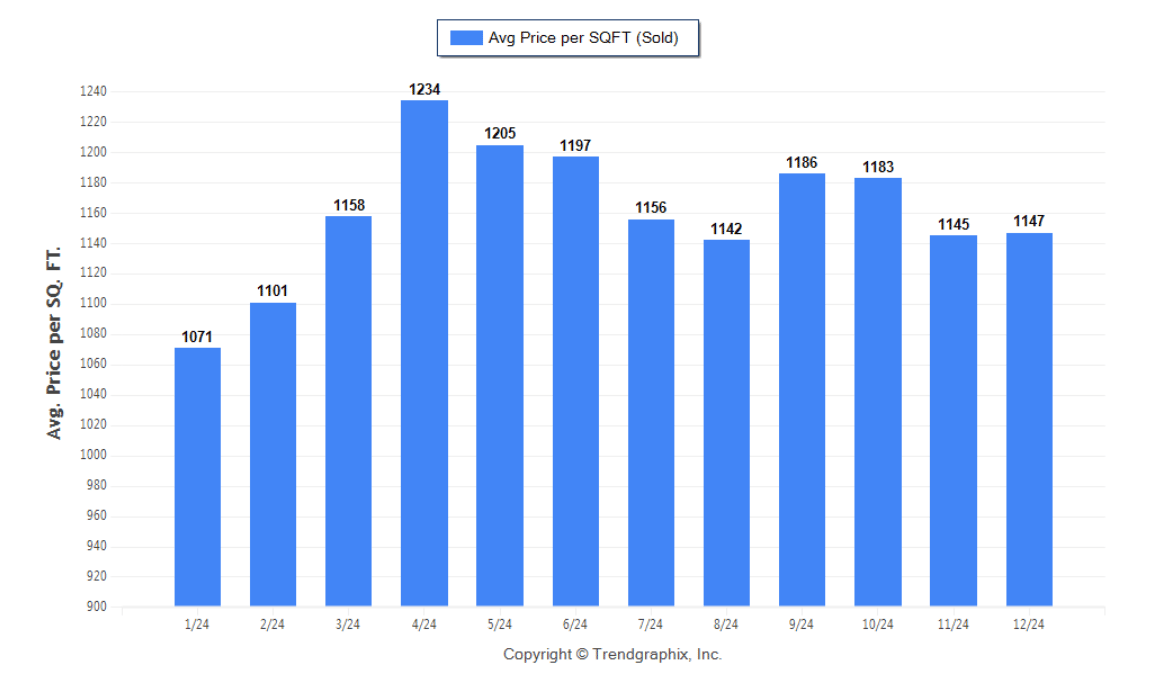

The above chart provides a comprehensive view of the average price per square foot of sold properties in Santa Clara County for the year 2024. Here's a detailed breakdown:

- January 2024 began with an average price of $1,071 per square foot, marking a relatively lower starting point for the year.

- The prices steadily increased in the first quarter, with February at $1,101 per square foot and March at $1,158 per square foot.

- April 2024 experienced a significant peak, reaching the highest average of the year at $1,234 per square foot, reflecting heightened demand or a shift in market dynamics.

- The trend slightly tapered off in the second quarter, with May and June averaging $1,205 and $1,197 per square foot, respectively, while still maintaining strong figures.

- A slight dip occurred in July at $1,156 per square foot, followed by August at $1,142 per square foot, indicating potential seasonal fluctuations or changing buyer behavior.

- The market rebounded in September and October, with averages of $1,186 and $1,183 per square foot, showcasing continued interest in the market.

- November and December closed the year at $1,145 and $1,147 per square foot, reflecting stability as the market settled toward year-end.

This data highlights a dynamic year for Santa Clara County's real estate market, with prices experiencing notable highs in the spring and steady demand through the fall. Understanding these trends can help buyers and sellers make informed decisions in 2024.

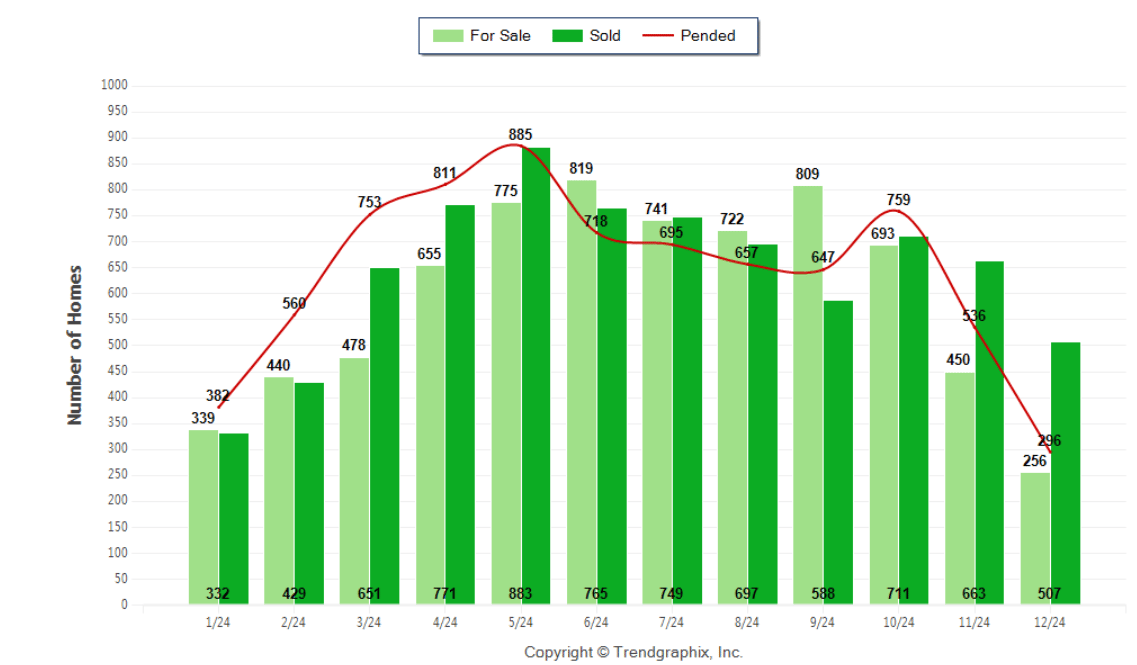

The above chart provides an overview of the Santa Clara County housing market in 2024, focusing on the number of homes For Sale, Sold, and Pended throughout the year. Here's a summary of the trends:

-

For Sale: The inventory of homes for sale saw a significant rise during the spring and summer months, peaking in May 2024 with 885 homes for sale. After this peak, inventory gradually decreased through the second half of the year, ending with only 296 homes for sale in December 2024.

-

Sold: The number of sold homes closely mirrored the trends in inventory, with sales reaching their highest point in May 2024 at 883 homes sold. This indicates strong buyer activity during the spring market. Sales gradually declined toward the end of the year, dropping to 256 homes sold in December 2024.

-

Pended: The number of homes pended (under contract) followed a similar trajectory, starting at 382 homes in January, peaking at 775 homes in April, and tapering off toward the year-end to 507 homes in December.

This data highlights the typical seasonality of the real estate market, with increased activity during the spring and summer months and a slowdown toward the end of the year. It underscores the importance of timing for both buyers and sellers, as inventory and buyer demand fluctuate throughout the year.

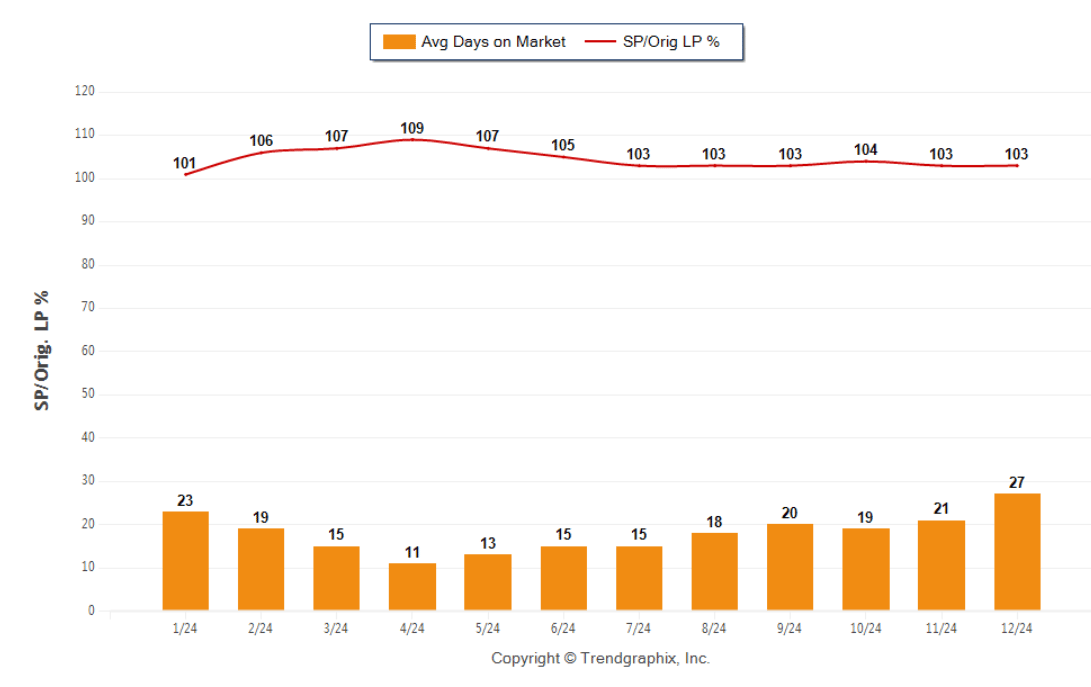

This above chart highlights two key metrics for the Santa Clara County real estate market in 2024: Average Days on Market (DOM) and the Sale Price to Original List Price (SP/Orig. LP%) ratio.

-

Average Days on Market: Homes generally sold quickly in 2024, with the lowest average DOM of 11 days in April, reflecting a highly competitive spring market. The DOM increased slightly during the latter half of the year, peaking at 27 days in December, which is typical as market activity slows during the holiday season.

-

SP/Orig. LP%: The ratio remained consistently strong throughout the year, averaging between 101% and 109%, indicating that most homes sold above their original list price. The highest percentage, 109%, occurred in March, reflecting heightened demand and buyer competition in the early spring market.

Overall, the data shows a robust market in 2024, with fast sales and strong buyer demand pushing sale prices above listing prices, especially during the peak spring and summer months. This trend underscores the importance of pricing strategies and timing in the Santa Clara County market.

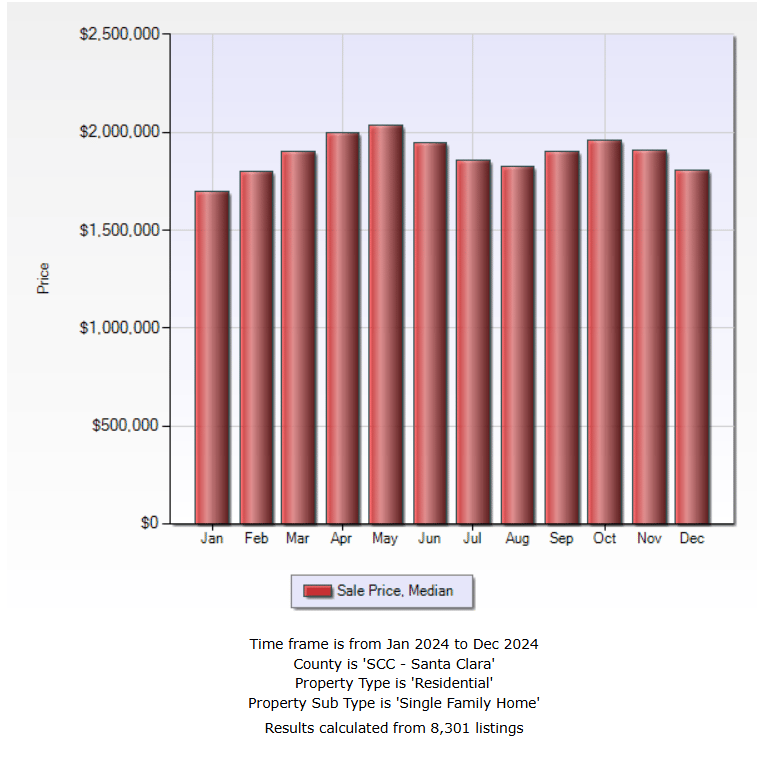

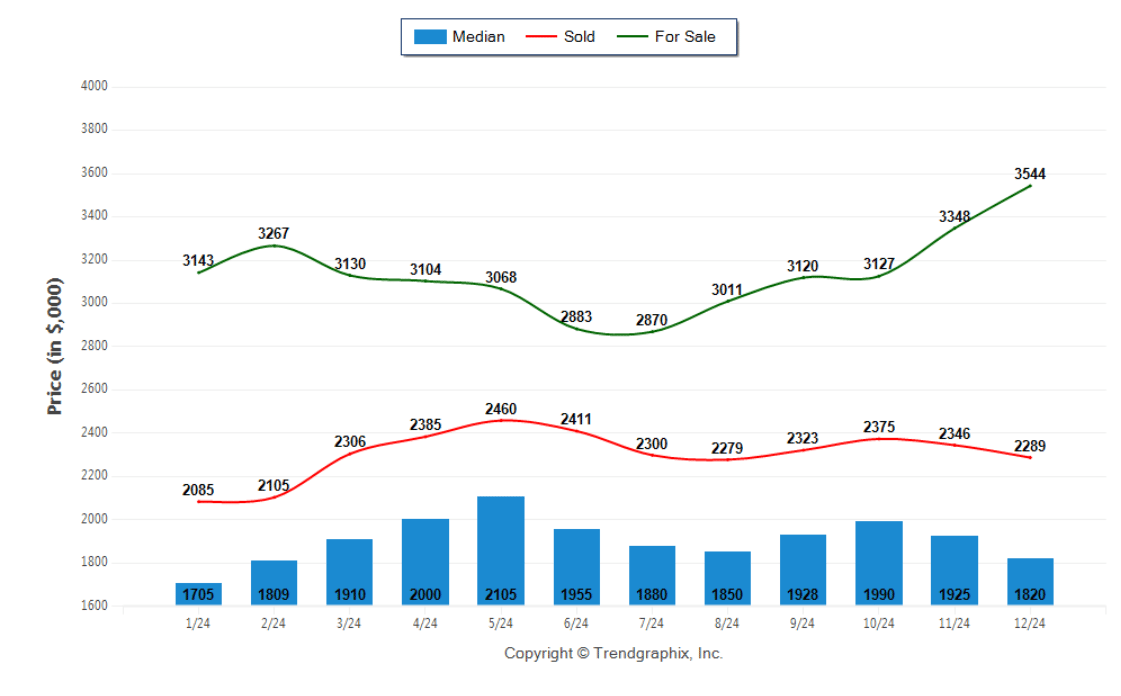

This above chart highlights three key pricing metrics for the Santa Clara County real estate market in 2024: Median Price, Sold Price, and For Sale Price. Here's a summary of the trends:

-

For Sale Price (Green Line): The price of homes listed for sale showed an upward trajectory throughout the year, starting at $3,143,000 in January and peaking at $3,544,000 in December. This steady increase reflects rising seller expectations or adjustments to market demand.

-

Sold Price (Red Line): The sold prices started lower at $2,085,000 in January, climbed steadily to a peak of $2,460,000 in May, and then gradually declined through the latter half of the year, ending at $2,289,000 in December. This reflects seasonal trends and possibly a softening in buyer competition toward year-end.

-

Median Price (Blue Bars): The median price for homes closely mirrored the sold price trends, beginning at $1,705,000 in January, peaking at $2,105,000 in May, and tapering off to $1,820,000 in December. This consistent alignment indicates that most homes sold near their median price point.

This data highlights a competitive spring market with higher sales and price peaks, followed by a gradual market cooldown in the second half of the year. Sellers benefited from rising listing prices, while buyers saw a slightly more balanced market toward year-end. These insights are crucial for understanding price dynamics and timing in Santa Clara County's real estate market.

What is an Absorption Rate?

There are 2 kinds of Absorption Rate as follows:

- Absorption Rate based on Closed Sales (%)

Absorption Rate based on Closed Sales (%) = the number of properties sold divided by the number of properties for sale (in percentage).

For instance, if there are 1,000 active listings and 100 of them sold in a given month, the rate of absorption would be 10%. 10% of the market is being sold in that given month. - Absorption Rate based on Pended Sales (%)

Absorption Rate based on Pended Sales (%) = the number of properties pended divided by the number of properties for sale (in percentage).

Rate of Absorption measures the inverse of Months of Inventory and represents how much of the current active listings (as a percentage) are being absorbed (sold or pended) each month. Absorption Rate is presented as a percentage (%) of the current inventory.

How to Use Months of Inventory Report?

As a rule of thumb, an absorption rate of less than 16.67% indicates a strong buyer market while an absorption rate level greater than 33.33% indicates a seller's market.

Buyer's market: 16.67% and below based on closed sales

Seller's market: 33.33% and above based on closed sales

Neutral market: 16.67% - 33.33% based on closed sales

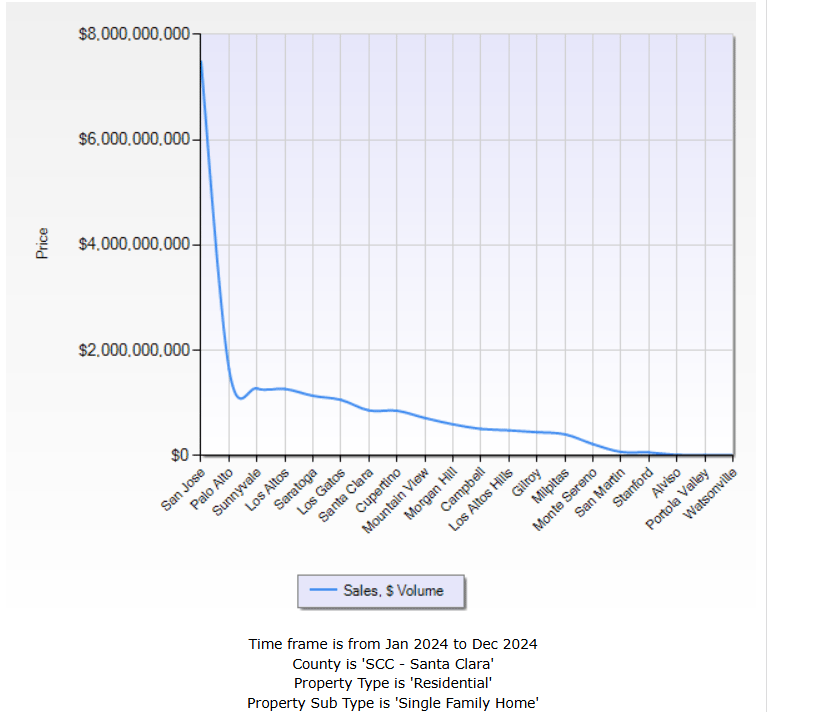

SALES VOLUME BY AREA